Inside the Digital Transformation of Loan Recovery Operations at a Mid-Sized Indian Cooperative Bank

When Traditional Recovery Methods Stop Working

India's cooperative banking sector has long been the financial backbone of small businesses, farmers, and salaried professionals in tier-2 and tier-3 cities. But as lending portfolios grow and borrower profiles become more complex, the cracks in manual recovery processes become impossible to ignore.

For one mid-sized cooperative bank based in Maharashtra, this reality hit hard. Rising non-performing assets (NPAs), an overworked collections team, and a patchwork of spreadsheets and phone calls had become the norm. What the bank needed wasn't just a software upgrade — it needed a fundamental rethink of how loan recovery operations worked from the ground up.

That shift came through the implementation of Smart Debt Collection, a purpose-built loan recovery software designed specifically for the operational realities of Indian lending institutions. This case study explores what changed, how it changed, and what the results looked like twelve months after go-live.

Client Background

Founded over four decades ago, this cooperative bank serves a member base of more than 180,000 borrowers spread across 24 branches in Maharashtra. Its lending portfolio spans personal loans, agricultural credit, MSME working capital, and housing finance — a diverse mix that brings its own set of recovery challenges.

Regulated under the Maharashtra Co-operative Societies Act and subject to Reserve Bank of India (RBI) guidelines for urban cooperative banks, the institution operates in a tightly governed environment where compliance isn't optional. Yet its internal recovery workflows had barely evolved in years — still dependent on manual follow-up calls, physical demand notices, and team-level Excel trackers that offered little visibility across branches.

By early 2023, the bank's NPA ratio had climbed to 7.2% — well above the internal benchmark of 4.5%. Leadership recognized that the problem wasn't the collections team; it was the absence of a structured, technology-driven recovery framework.

The Challenges: Where the Process Was Breaking Down

Fragmented Recovery Workflows

With 24 branches operating largely independently, there was no centralized view of overdue accounts. Branch managers maintained their own tracking methods, leading to inconsistencies in follow-up frequency, escalation timelines, and documentation quality. Accounts that needed urgent attention often slipped through the cracks simply because no one system flagged them.

Heavy Reliance on Manual Processes

Recovery agents were spending an estimated 60% of their working hours on non-recovery tasks — logging call outcomes in spreadsheets, drafting manual notices, updating branch registers, and preparing weekly reports for senior management. This left less than half their time available for actual borrower engagement and negotiation.

Compliance and Audit Gaps

Meeting RBI's fair practices code for loan recovery required meticulous documentation of every borrower interaction. In practice, this was inconsistently done. When audit queries arose, the team had to manually compile records from multiple sources — a time-consuming and error-prone process that created unnecessary regulatory exposure.

Poor Visibility for Management

Branch-level recovery data reached senior leadership only through weekly Excel summaries, which were often outdated by the time they arrived. There was no real-time dashboard, no early warning system for deteriorating accounts, and no way to compare recovery performance across branches objectively.

Unstructured Communication with Borrowers

Follow-up communications — calls, SMS reminders, and notices — were handled ad hoc, with no standardized cadence or escalation logic. Some borrowers received multiple contacts in a single week while others went weeks without any outreach, creating both borrower dissatisfaction and missed recovery opportunities.

The Solution: Implementing Smart Debt Collection

After evaluating several loan recovery software options available in the Indian market, the bank selected Smart Debt Collection for its combination of configurable workflows, RBI compliance features, and its ability to integrate with the bank's existing core banking system (CBS).

The implementation was carried out in phases over 14 weeks, with dedicated onboarding support, staff training, and a parallel-run period to ensure continuity of operations.

Centralized Recovery Dashboard

Smart Debt Collection gave branch managers and senior leadership a single, real-time view of the entire recovery pipeline. Overdue accounts were automatically classified by bucket — 0–30 DPD, 31–60 DPD, 61–90 DPD, and NPA — with color-coded risk indicators and automated escalation triggers. For the first time, management could compare branch-level performance on a single screen.

Automated Follow-Up Workflows

The software's workflow engine replaced manual outreach with a structured communication cadence. SMS reminders, auto-generated demand notices, and agent call assignments were triggered automatically based on account status and days past due. Agents received daily task queues rather than unstructured to-do lists, and every action was logged against the borrower's account in real time.

RBI-Compliant Documentation and Audit Trails

Smart Debt Collection maintained a complete, timestamped audit trail for every borrower interaction — call logs, notice dispatches, field visit reports, and settlement discussions. This not only simplified internal audits but also ensured full compliance with RBI fair practices guidelines without adding manual documentation overhead.

Integrated Reporting and Analytics

Managers could generate branch-wise, agent-wise, and bucket-wise recovery reports on demand. Predictive indicators highlighted accounts at risk of further deterioration, allowing teams to prioritize proactively rather than reactively. Monthly board-level recovery summaries — previously a two-day manual effort — were now available in under 30 minutes.

Field Agent Mobile Application

Recovery agents in the field were equipped with the Smart Debt Collection mobile app, which gave them access to borrower histories, geo-tagged visit logging, digital payment collection, and instant acknowledgment generation. This eliminated the need for paper-based field records and significantly reduced the turnaround time for updating head office on field outcomes.

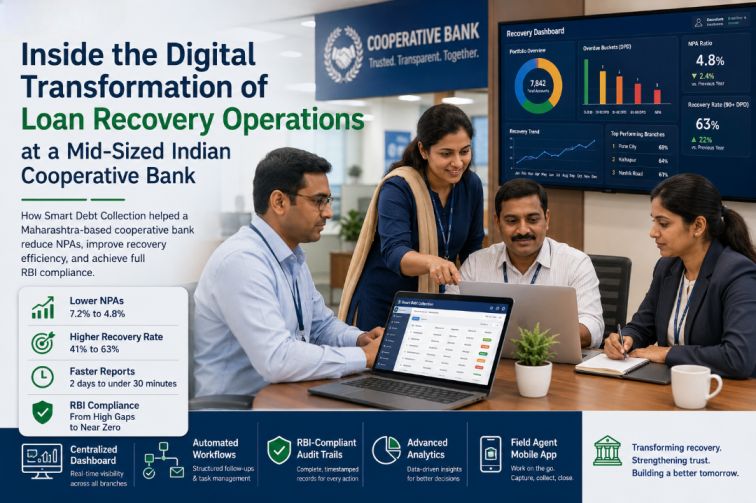

Results and Business Impact

Twelve months after full deployment, the bank conducted an internal performance review comparing pre- and post-implementation metrics. The results were significant across every measured dimension.

Performance Metric | Before | After (12 Months) |

NPA Ratio | 7.2% | 4.8% |

Recovery Rate (90+ DPD) | 41% | 63% |

Agent Productive Time on Recovery | ~40% | ~74% |

Monthly Report Generation Time | 2 days | Under 30 minutes |

Average Notice Dispatch Turnaround | 4–5 days | Same day (automated) |

Compliance Documentation Gaps (Audit) | High | Near zero |

Branch Performance Visibility | Weekly, manual | Real-time dashboard |

Beyond the numbers, the collections team reported a measurable improvement in day-to-day working conditions. Agents spent less time on paperwork and more time on meaningful borrower engagement. Branch managers felt more confident in their account oversight, and senior leadership had the data they needed to make faster, better-informed decisions on restructuring and write-offs.

The reduction in NPA ratio from 7.2% to 4.8% within 12 months — while not solely attributable to the software alone — represented a significant financial improvement. Combined with faster recovery cycles and reduced operational overhead, the bank's collections function effectively paid for the implementation cost within the first year.

Key Takeaways

This case study illustrates a transformation that many mid-sized Indian cooperative banks and NBFCs are now facing: the gap between growing portfolio complexity and aging operational infrastructure. A few lessons stand out clearly.

- Automation doesn't replace good recovery agents — it amplifies them. By removing repetitive administrative tasks, Smart Debt Collection freed the bank's team to focus on what actually drives recovery: meaningful borrower conversations and timely escalation.

- Compliance and efficiency are not trade-offs. A well-implemented loan recovery software makes regulatory compliance a natural outcome of the process rather than an afterthought that requires separate effort.

- Real-time visibility changes leadership behaviour. When branch performance data is available instantly, management can intervene earlier and allocate resources more effectively — a capability that weekly Excel reports simply cannot replicate.

- Digital transformation in Indian cooperative banking is not about replacing tradition — it's about building the operational infrastructure to serve growing borrower bases without proportionally growing overheads.

For this Maharashtra-based cooperative bank, Smart Debt Collection became more than a tool — it became the operational backbone of a fundamentally improved collections function.

Conclusion

India's lending landscape is evolving rapidly. Borrower expectations, regulatory requirements, and portfolio scales are all increasing simultaneously — and manual recovery processes are simply not built to handle this complexity at scale.

This case study demonstrates what's possible when a mid-sized institution makes a deliberate, well-supported shift to purpose-built loan recovery software. The results — a 22-percentage-point improvement in recovery rates, a near-elimination of compliance gaps, and a dramatic reduction in administrative overhead — speak to the practical, measurable impact of getting the technology right.

For cooperative banks, NBFCs, and lending institutions across India that are still navigating recovery operations through spreadsheets and manual processes, the message is straightforward: the tools to do this better already exist. The question is how long you can afford to wait.

Ready to modernize your loan recovery operations? Explore how Smart Debt Collection can work for your institution.

Best loan recovery software in India

Best bank debt collection management software in India

Best debt recovery management software in India

If you need a free demo on the best loan recovery software in India, please fill out the form below.